America is rapidly moving toward a cashless future powered by mobile wallets, contactless payments, fintech innovation, and digital-first banking. This in-depth guide explores why U.S. cities are phasing out cash, how digital payments are redefining everyday life, and what Americans must do now to prepare. Learn about risks, benefits, CBDCs, real-world examples, and the future of financial access in a digitally connected economy.

Introduction

Across the United States, a major shift is unfolding—one that affects how every American buys groceries, pays for transportation, shops online, covers bills, and even receives income. Cash, once the cornerstone of everyday commerce, is slowly but steadily being replaced by digital alternatives. A combination of fintech innovation, consumer demand, and big tech ecosystem integration has put the nation on a fast track toward a predominantly cashless society.

In many cities, you can already go days or weeks without touching a single dollar bill. Mobile wallets, tap-to-pay cards, real-time payment systems, and digital banking platforms are accelerating the shift. Younger generations already prefer it. Businesses find it cheaper. Governments find it more efficient. And consumers—often without realizing it—are participating in the biggest transformation in the history of American money.

But as this shift accelerates, important questions emerge:

- Why are more businesses refusing cash?

- Is a cashless society safe?

- Will digital wallets replace banks?

- Does this hurt people who rely on cash?

- What happens when everything depends on a smartphone?

This long-form guide answers all of these questions and more. It will help you understand the forces driving a cashless America, the risks and rewards involved, and what you should be doing right now to prepare your wallet—and your financial life—for what’s next.

Why Are American Cities Moving Toward a Cashless Future?

The shift isn’t accidental. It’s driven by powerful technology, business, and consumer trends that have changed the way America spends money.

1. Digital payments are faster, easier, and more convenient

Mobile wallets and tap-to-pay cards have fundamentally changed consumer behavior. Digital payments are:

- Instant

- Contactless

- Easier to track

- Simpler for budgeting

- Available through smartphones most Americans already use

A recent Pew Research Center study found that 41% of Americans say they now go entire weeks without using cash, up from 24% in 2015. The trend grows every year.

2. Businesses save billions by reducing cash-handling

Cash isn’t free for businesses. It requires:

- Safes and cash drawers

- Extra staff training

- End-of-day reconciliation

- Armored truck pickups

- Theft prevention

- Counterfeit detection

Digital payments dramatically reduce these costs, making them more attractive to merchants.

3. Mobile wallets dominate for younger generations

Apple Pay, Google Wallet, Cash App, Venmo, PayPal, and other digital wallets have become everyday tools. More than 150 million Americans use mobile payments monthly, according to various industry reports.

4. COVID-19 normalized contactless everything

During the pandemic, contactless payments surged, with businesses rapidly adopting digital systems to reduce physical interaction. It changed consumer expectations permanently.

5. New technology like FedNow accelerates digital adoption

The launch of FedNow in 2023 created a national instant-payment infrastructure. This system makes digital transfers faster, cheaper, and more reliable than ever—reducing the need for physical cash.

Which U.S. Cities Are Leading the Cashless Revolution?

Some American cities are further along than others. But almost all major metros are moving toward cashless operations in some form.

New York City

Although laws require many businesses to still accept cash, an increasing number of restaurants, cafés, and event venues now operate primarily through digital payments.

San Francisco & Silicon Valley

Tech-forward businesses, transit systems, and events often run completely cash-free, reflecting the Bay Area’s innovation culture.

Seattle

From boutique coffee shops to public transit, Seattle has embraced digital payments faster than most U.S. cities.

Austin

As a growing tech hub, Austin’s food trucks, micro-retail spaces, music festivals, and events frequently go cashless.

Las Vegas

Casinos, venues, and entertainment spaces increasingly use digital wallets for chips, payments, and ticketing.

The bottom line:

Nearly every major U.S. city has already taken steps toward a heavily cashless environment.

Will America Become 100% Cashless?

This is one of the most common questions consumers now search online.

The realistic answer: No.

America will not eliminate cash entirely, but it will become predominantly cashless, meaning:

- 80%–95% of daily transactions will be digital

- Cash will exist mostly for emergencies, seniors, rural areas, and specific use cases

- Businesses will be allowed—or required—to accept some cash, depending on state laws

But the nation’s money ecosystem is undeniably shifting toward digital-first transactions.

How a Cashless America Will Change Everyday Life

The transition impacts nearly every aspect of daily living. Here’s what you’ll notice most:

1. Faster transactions everywhere

Lines move more quickly when nobody exchanges bills or coins. This is already visible at:

- Stadiums

- Fast-food restaurants

- Grocery stores

- Subway and bus stations

- Parking meters

2. Real-time budgeting becomes easier

Digital payments generate data. That data powers:

- Spend categorizations

- Bill reminders

- Budget forecasts

- Automatic savings transfers

- Overspending alerts

Banks didn’t offer this level of insight in the past—but fintech apps now do it automatically.

3. Government services become more efficient

Many U.S. cities already require digital payments for:

- Parking

- Toll roads

- Utility bills

- DMV services

- Court fees

In a cashless future, this will only expand.

4. Borrowing becomes more accurate and inclusive

Fintech lenders use cash-flow analytics instead of outdated credit models. This benefits:

- Gig workers

- Freelancers

- Young adults

- Immigrants

- People with thin credit files

A cashless society produces more reliable financial data, making borrowing faster and more fair.

5. More Americans gain access to digital banking

Millions who once relied on check-cashing stores or physical banks can now open digital accounts with:

- No minimum balances

- No overdraft fees

- Early paycheck access

- Mobile-only onboarding

Digital-first finance creates new pathways to inclusion.

What Happens to Americans Who Still Depend on Cash?

This is one of the biggest concerns among policymakers.

Groups most affected include:

- Seniors

- Low-income households

- People without smartphones

- Undocumented workers

- Rural communities

Some states and cities have responded with cash acceptance laws. These regulations require certain businesses and public services to accept cash.

Yet even with protections in place, digital payments continue taking over. Consumers who rely solely on cash may face increasing challenges in coming years.

Is a Cashless Future Safe?

Going cashless brings advantages—but also introduces new risks.

Pros

- No risk of cash theft

- Transactions easily documented

- Better budgeting tools

- Reduced business losses

- Faster checkout

Cons

- Privacy concerns

- Technology dependence

- Potential network outages

- Cybersecurity threats

- Increased data tracking

Real Example

In 2021, a major payment processor outage temporarily prevented millions of Americans from using cards or digital wallets.

This event highlighted the need for digital redundancy and backup systems.

Still, digital payments—protected by tokenization, biometrics, and encryption—generally experience lower fraud rates than physical cash or cards.

Where Do CBDCs Fit Into the Cashless Movement?

A Central Bank Digital Currency (CBDC) is being studied by the Federal Reserve as a possible digital complement to the U.S. dollar.

Most Americans now ask:

“Will CBDCs replace cash?”

Unlikely.

CBDCs would act alongside cash—not replace it outright.

Benefits might include:

- Faster government payments

- Lower transaction costs

- Enhanced financial inclusion

- More secure digital infrastructure

A CBDC could accelerate America’s shift into a digital-first monetary system.

How You Can Prepare for a Cashless Future

Here are practical steps to future-proof your wallet:

✔ Set up multiple digital payment methods

Use Apple Pay, Google Pay, PayPal, Cash App, and debit/credit cards.

✔ Use a digital-first bank or fintech platform

These offer better yields, zero-fee accounts, and faster processing.

✔ Turn on fraud alerts and security features

Biometric verification significantly reduces risk.

✔ Keep a small emergency cash reserve

Digital outages are rare—but they happen.

✔ Learn QR-based payments

These are expanding in restaurants, transit, and retail.

✔ Automate recurring payments

Digital living works best when essential bills run automatically.

Real-Life Scenarios of Cashless America

1. Cashless Stadiums

Events at NFL and NBA arenas increasingly accept only cards or digital wallets, speeding up lines dramatically.

2. Digital Public Transit

Cities like New York and Chicago allow riders to tap in with smartphones or cards—no more purchasing physical tickets.

3. Cashless Cafés

Boutique coffee shops nationwide now run digital-only payment systems, reducing staff costs and errors.

4. Cashless Allowances for Kids

Apps like Greenlight and GoHenry help kids manage digital money with parental oversight.

Each scenario offers a glimpse of the near future for every American city.

10 Frequently Asked Questions (FAQs)

1. Will the United States ever eliminate cash completely?

No. Cash will remain but will become less commonly used for everyday transactions.

2. Is a cashless society safer than one with cash?

It reduces robbery and theft but increases reliance on cybersecurity and technology.

3. What happens during a digital payment outage?

Multiple payment methods and backup cards help minimize disruption.

4. How does a cashless society affect seniors?

Some seniors struggle with digital tools, which is why many cities mandate cash acceptance.

5. Are digital payments more expensive?

Typically no. Many fintech platforms offer zero-fee services.

6. Will CBDCs replace bank accounts?

No. CBDCs would likely operate through existing banks and fintech apps.

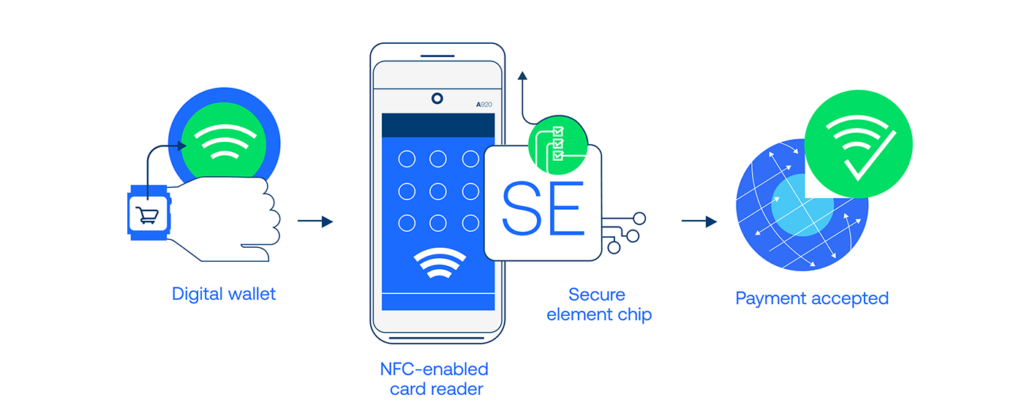

7. Are mobile wallets secure?

Yes. They use encryption, biometrics, and tokenization—safer than traditional card swipes.

8. What’s the biggest risk in going cashless?

Privacy and increased data collection.

9. How does going cashless help businesses?

Lower costs, fewer errors, faster lines, and reduced theft.

10. How can low-income individuals transition safely?

Through prepaid debit cards, digital-first bank accounts, community banking programs, and mobile-accessible financial literacy tools.