The Federal Reserve’s upcoming policy decisions may dramatically impact retirement savings, investment growth, and long-term financial security for millions of Americans. This comprehensive guide explains how interest rate changes, inflation trends, and balance sheet strategies could affect 401(k)s, IRAs, and other retirement accounts. Readers will find actionable strategies, real-life examples, and expert-backed insights to protect their nest egg amid economic uncertainty.

Understanding the Fed’s Influence on Retirement

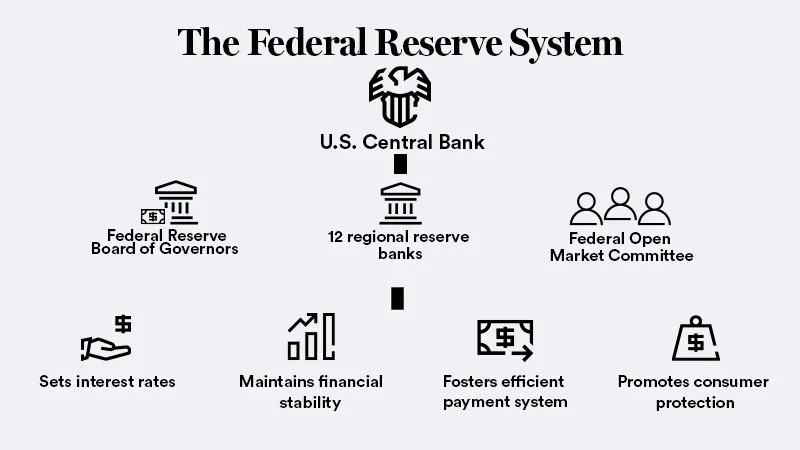

The Federal Reserve (the Fed) wields tremendous influence over the U.S. economy through its monetary policy, primarily by adjusting interest rates, controlling inflation, and regulating credit availability. While these actions are meant to stabilize the economy, they can unintentionally affect individual retirement plans, particularly for those invested heavily in stocks, bonds, and fixed-income instruments.

Why retirees and pre-retirees should care:

Even small Fed actions ripple through the markets. Higher rates can slow stock growth, alter bond yields, and reduce purchasing power. According to the Investment Company Institute, over 55 million Americans hold employer-sponsored retirement accounts, meaning a significant portion of the population could be exposed to Fed policy shifts.

How the Fed’s Moves Affect Retirement Accounts

1. Interest Rate Changes and Retirement Savings

The Fed adjusts the federal funds rate to control inflation and stimulate or cool the economy. The effects on retirement portfolios are significant:

- High rates: Increase borrowing costs, potentially slowing economic growth. Stocks may decline, affecting 401(k) balances. Bonds offer higher yields, but existing holdings may lose market value.

- Low rates: Encourage borrowing and investment but may reduce returns on savings accounts, CDs, and other fixed-income options.

Real-life example:

In 2018, rapid rate hikes caused bond markets to adjust, temporarily lowering returns for retirees relying on fixed-income funds, forcing some to postpone withdrawals.

2. Inflation and Purchasing Power

Inflation erodes the value of money over time. When the Fed miscalculates or delays interventions, retirees may find that their monthly budgets are increasingly strained, even if nominal account balances appear stable.

Example:

A retiree holding $500,000 in cash-equivalent investments might see the purchasing power of that money decline by 10–15% over three years if inflation outpaces returns.

3. Stock Market Volatility

The stock market reacts strongly to Fed signals. Interest rate adjustments often trigger sudden shifts:

- Rising rates generally depress stock valuations.

- Falling rates can fuel short-term rallies, though sustainability is not guaranteed.

Retirees near withdrawal age are especially vulnerable since losses are harder to recover compared to younger investors.

Practical Implications for Retirees

Many retirees rely on a mix of stocks, bonds, and cash. Fed moves directly influence each asset class:

- Stocks: Potential sudden drops in portfolio value.

- Bonds: Higher yields for new issues, but falling market values for existing bonds.

- Cash savings: Inflation diminishes real purchasing power.

Expert insight: According to Fidelity Investments, diversification and strategic asset allocation are crucial for mitigating Fed-driven risks.

How to Protect Your Retirement Against Fed Risks

While individual investors cannot control the Fed, strategic planning can reduce vulnerability.

Actionable strategies:

- Diversify across equities, bonds, real estate, and alternative investments.

- Include inflation-protected securities (e.g., TIPS) in fixed-income allocations.

- Adjust withdrawal strategies during market volatility.

- Consider short-duration bonds to reduce exposure to interest rate changes.

- Maintain emergency funds outside volatile accounts to avoid forced withdrawals.

Real-life case:

A 62-year-old retiree with a 50/50 stock/bond allocation shifted 20% of bonds to TIPS during a rising-rate period, preserving portfolio value and mitigating purchasing power losses.

Fed Signals to Watch in 2025

Key indicators hinting at future Fed actions:

- Rate hikes or cuts announced at FOMC meetings.

- Balance sheet adjustments via quantitative tightening or easing.

- Inflation metrics like CPI and PCE indexes.

- Employment and wage trends, affecting overall economic momentum.

Monitoring these indicators allows retirees to rebalance portfolios proactively, rather than reactively.

Signs Your Retirement Could Be At Risk

Certain conditions increase vulnerability to Fed policy shifts:

- Stock-heavy portfolios with minimal diversification.

- Large cash positions earning below-inflation returns.

- Heavy exposure to long-duration bonds susceptible to rising rates.

- Dependence on predictable monthly withdrawals without contingency plans.

Example:

During the 2022 inflation surge, retirees reliant on long-term bond funds saw returns erode, forcing delayed discretionary spending and budget adjustments.

FAQs: How the Fed Affects Retirement

1. How does a Fed rate hike affect my 401(k)?

Higher rates may depress stock valuations and temporarily reduce portfolio growth, but bond yields may improve over time.

2. Should I move money out of stocks when rates rise?

Not necessarily. Diversification and a long-term perspective are more effective than panic selling.

3. Are fixed-income investments safe from Fed actions?

They are affected by interest rates; short-duration bonds and inflation-protected securities help mitigate risks.

4. Can the Fed reduce my retirement income?

Indirectly, yes. Lower portfolio growth and inflation erosion can reduce purchasing power and affect withdrawals.

5. How do I protect my savings from inflation?

Consider TIPS, commodities, diversified assets, and avoid concentrating all funds in cash.

6. Is it better to retire early or wait if the Fed is raising rates?

Waiting may allow time to adjust portfolios, but personal financial needs and market conditions should guide decisions.

7. How often should retirees monitor the Fed?

At least quarterly, focusing on FOMC announcements and inflation reports relevant to your investments.

8. Can real estate investments offset Fed-driven risks?

Potentially, as property values and rental income may rise during certain rate environments.

9. Does the Fed impact Social Security or pensions?

Not directly, but inflation adjustments to benefits and pension fund investments can be affected.

10. What’s the safest approach for retirees during Fed uncertainty?

Diversification, professional financial guidance, and maintaining liquid reserves for emergencies.

Real-Life Stories of Fed Impact on Retirees

Jane, 67, Retired Teacher

Jane’s portfolio lost 7% after a surprise 2019 rate hike. By reallocating some funds to TIPS and dividend stocks, she maintained withdrawals without touching principal.

Mark, 62, Engineer

Mark relied heavily on corporate bonds. During Fed tightening, the bonds lost value. He shifted to shorter-term securities and some equities, reducing risk exposure.

Susan, 70, Consultant

Susan kept excess cash in savings, which lost purchasing power to inflation. Reinvesting in low-risk equities and TIPS preserved her lifestyle.

Key Takeaways

- The Fed’s policy decisions directly affect stocks, bonds, and cash assets.

- Retirement portfolios are vulnerable to rate hikes and inflation surges.

- Diversification and proactive management reduce risk exposure.

- Monitoring Fed signals allows for strategic portfolio adjustments.

- Real-life examples show preparation protects both wealth and lifestyle.

Retirement planning now requires understanding macroeconomic forces like Fed policy and aligning portfolios to balance growth with safety.

")

")